Scarcity, Choice and Resource Allocation - Theme 1.1.1 Economics Notes

Free downloadable A Level H2 Economics Notes. Topic 1.1.1 covers scarcity, choice and opportunity cost, starting at the foundation of Economics. Learn the factors of production, the PPC, and how economic agents make trade-offs.

H2 Economics (9570) · Theme 1 · The Central Economic Problem

1.1.1 Scarcity, Choice & Resource Allocation

Syllabus Requirements

| Code | Requirement |

|---|---|

| 1.1.1a | The Central Economic Problem is scarcity, arising from limited resources and unlimited wants |

| 1.1.1b | Scarcity implies that choices have to be made in the allocation of resources between different uses |

| 1.1.1c | When choices are made, trade-offs and opportunity costs are incurred |

| 1.1.1d | The concepts of scarcity, choice and opportunity cost can be explained from the perspectives of different economic agents (consumers, producers and governments) |

| 1.1.1e | Production Possibility Curve (PPC) can be used to illustrate scarcity, choice, opportunity cost, productive efficiency, full employment, unemployment or under-utilisation of economic resources, and changes in the productive capacity of an economy |

1.1.1a — The Central Economic Problem (Scarcity)

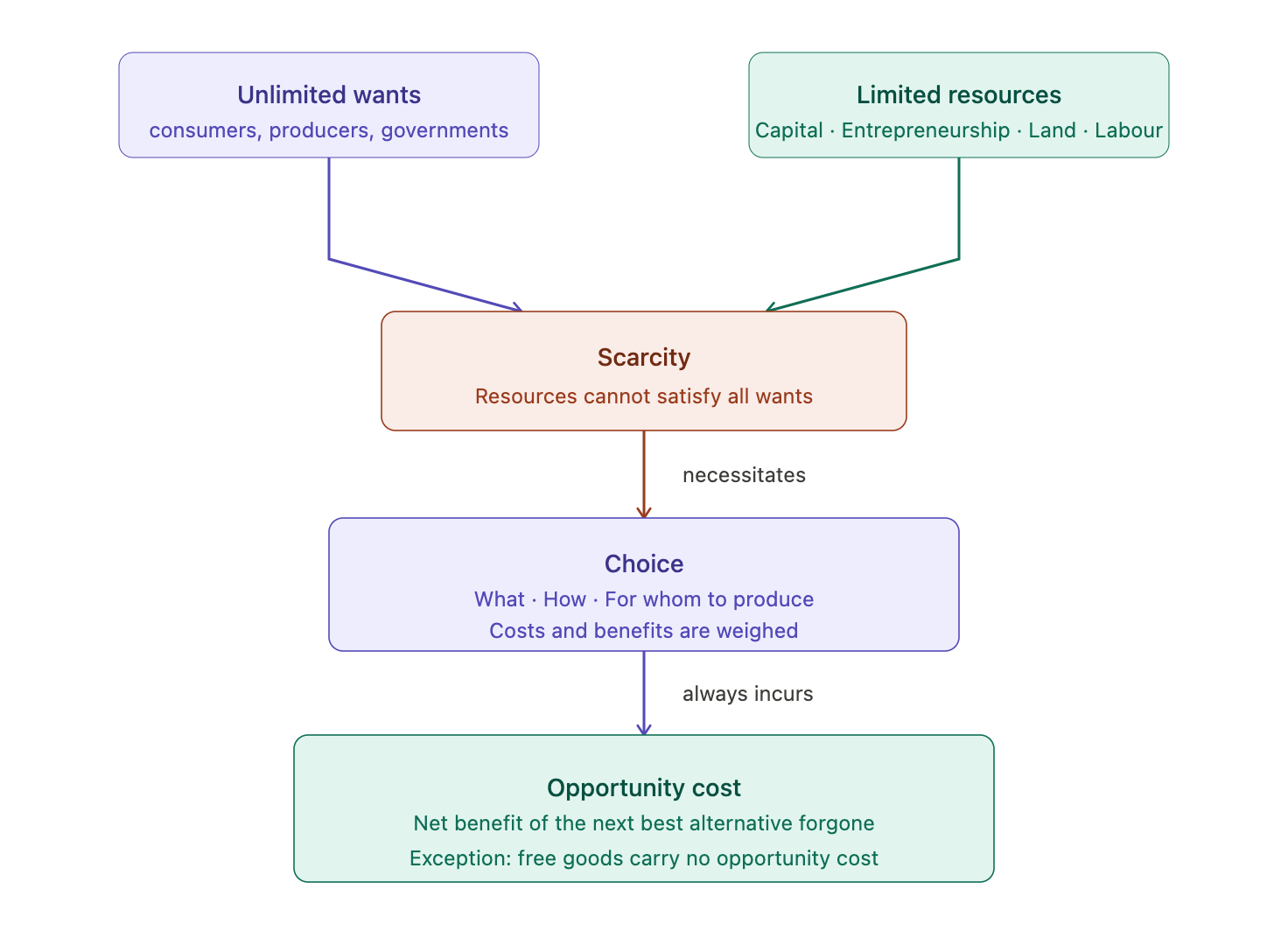

Definition: Scarcity is the fundamental economic problem arising because human wants are unlimited while the resources available to satisfy those wants are limited.

What are wants?

A want is a wish or desire to have something. Wants are effectively unlimited — as old wants are satisfied, new ones emerge.

Common mistake — Want ≠ Demand: A want becomes demand only when backed by both the willingness and ability to pay. Wants are broader than demand.

All three economic agents have unlimited wants:

- Consumers — want to consume more goods and services to maximise utility (satisfaction)

- Producers — want to produce more output and earn unlimited profits

- Governments — want to provide more public goods and services to citizens

Factors of production (CELL)

Resources are inputs used to produce goods and services. They are always finite relative to wants.

| Factor | Definition | Examples | Return |

|---|---|---|---|

| Capital | Man-made physical resources used in production | Machinery, factories, infrastructure, tools | Interest |

| Entrepreneurship | Human effort that organises land, labour and capital; bears risks | Business owners who innovate, make decisions and take risks | Profit |

| Land | All natural resources available to mankind. Includes both renewable and non-renewable sources | Renewable: wind, water, solar · Renewable (with management): forests, marine life · Non-renewable: fossil fuels, mineral ores | Rent |

| Labour | Human effort (mental and physical) from individuals who are willing and able to work. Limited by the 24-hour day | Workers, skilled professionals | Wages |

Memory aid: Remember factors of production with CELL — Capital, Entrepreneurship, Land, Labour

Scarcity ≠ Shortage: Scarcity is permanent — unlimited wants will always exceed limited resources. Shortage is temporary — supply is insufficient to meet demand at a given price, and can be resolved.

Key takeaways — 1.1.1a

- The Central Economic Problem is scarcity

- Scarcity arises from the conflict between unlimited wants and limited resources (CELL)

- Scarcity is universal — it affects all economies regardless of wealth or size

1.1.1b — Scarcity & Choice

Core idea: Because resources are scarce and have alternative uses, economic agents must make choices about how to allocate them. Scarcity necessitates choice.

The same piece of land can be used to build a hospital or a school; the same worker can be employed in manufacturing or agriculture. Because resources cannot be used for all purposes simultaneously, choices must be made.

The three fundamental economic questions

All economies — regardless of economic system — must answer:

| Question | What it asks |

|---|---|

| ① What & how much to produce? | Which goods and services to produce, and in what quantities? Producing more of one good means fewer resources are available for another. |

| ② How to produce? | Which method of production: labour-intensive or capital-intensive? The aim is to maximise output from a given amount of resources. |

| ③ For whom to produce? | Who receives the goods and services produced? Should distribution be based on ability to pay, or on need? |

Productive and allocative efficiency

- Productive efficiency — maximum possible output from a given amount of resources, or equivalently, a given output at the lowest possible cost.

- Allocative efficiency — resources produce the combination of goods that best reflects what society wants, maximising overall welfare.

Key takeaways — 1.1.1b

- Scarcity forces all economic agents to make choices about resource allocation

- Every economy must address: what, how, and for whom to produce

1.1.1c — Trade-offs & Opportunity Cost

Definition: Opportunity cost is the net benefit that could have been derived from the next best alternative forgone as a result of a decision made.

Common mistake: Opportunity cost = net benefit of the next best alternative forgone. It is NOT the sum of all alternatives forgone.

Trade-offs

A trade-off occurs when choosing one option means accepting less of something else. Because resources are scarce, every choice involves a trade-off — gaining more of one good requires sacrificing some of another.

How to determine opportunity cost

- Identify all available options

- Rank options by net benefit (total benefit minus total cost)

- Choose the highest-ranked option

- Opportunity cost = net benefit of the second-highest ranked option

Example: Sam has three job offers ranked by net benefit:

- Job A — $3,500/month ← chosen

- Job B — $3,000/month ← next best

- Job C — $2,800/month

Opportunity cost = net benefit of Job B = $3,000/month

Note: If non-monetary conditions differ (e.g. Job B offers better career prospects), those benefits must be factored in and the ranking may change.

Free goods = zero opportunity cost

Free goods exist in such abundance that consuming them imposes no opportunity cost on society. Examples: air, sunlight, sand in a desert.

Common mistake — Free goods ≠ free gifts: Promotional "free" offers required resources to produce — an opportunity cost is incurred. The word "free" here refers to the absence of scarcity, not the absence of a price tag.

Key takeaways — 1.1.1c

- Every choice involves a trade-off: gaining more of one thing requires giving up something else

- Opportunity cost = net benefit of the next best alternative forgone

- Rational agents choose the option with the highest net benefit

- Free goods are the only exception — no scarcity means no opportunity cost

1.1.1d — Perspectives of Economic Agents

| Economic agent | Objective | Example of scarcity | Example of opportunity cost |

|---|---|---|---|

| Consumers | Maximise utility | Limited income relative to wants | $500 on a phone → forgone satisfaction from next best use (e.g. new clothes) |

| Producers | Maximise profits | Limited factors of production | Land used for a factory → forgone revenue from next best use (e.g. growing crops) |

| Government | Maximise social welfare | Limited national budget | $3M on hospitals → forgone social welfare from next best use (e.g. building schools) |

Positive vs normative economics

| Type | Definition | Key feature | Example |

|---|---|---|---|

| Positive | Describes and explains economic phenomena based on facts and cause-effect relationships | Value-free; can be tested/verified against evidence | "An increase in household income will increase demand for luxury goods." |

| Normative | Expresses value judgements about what the economy ought to be | Contains value judgement; cannot be proven or disproven by facts alone | "The government should subsidise car production." |

Exam tip: Look for "should", "ought to", "fairer", "better" → Normative. A testable factual claim → Positive.

Watch for disguised normative statements. "Higher taxes on cigarettes are the fairest way to reduce smoking" sounds factual, but "fairest" reveals a value judgement.

Exam point: A positive statement can be factually wrong and still be positive. "An increase in income causes demand to fall" is testable — even though it is incorrect for normal goods. What makes a statement positive is that it is testable, not that it is true.

Key takeaways — 1.1.1d

- Scarcity, choice and opportunity cost apply to all three agents, but constraints differ

- Consumers face limited income; producers face limited factors of production; governments face limited budgets

- Positive statements are value-free and testable; normative statements contain value judgements

- A statement can be positive even if factually wrong — what matters is whether it can be tested

1.1.1e — Production Possibility Curve (PPC)

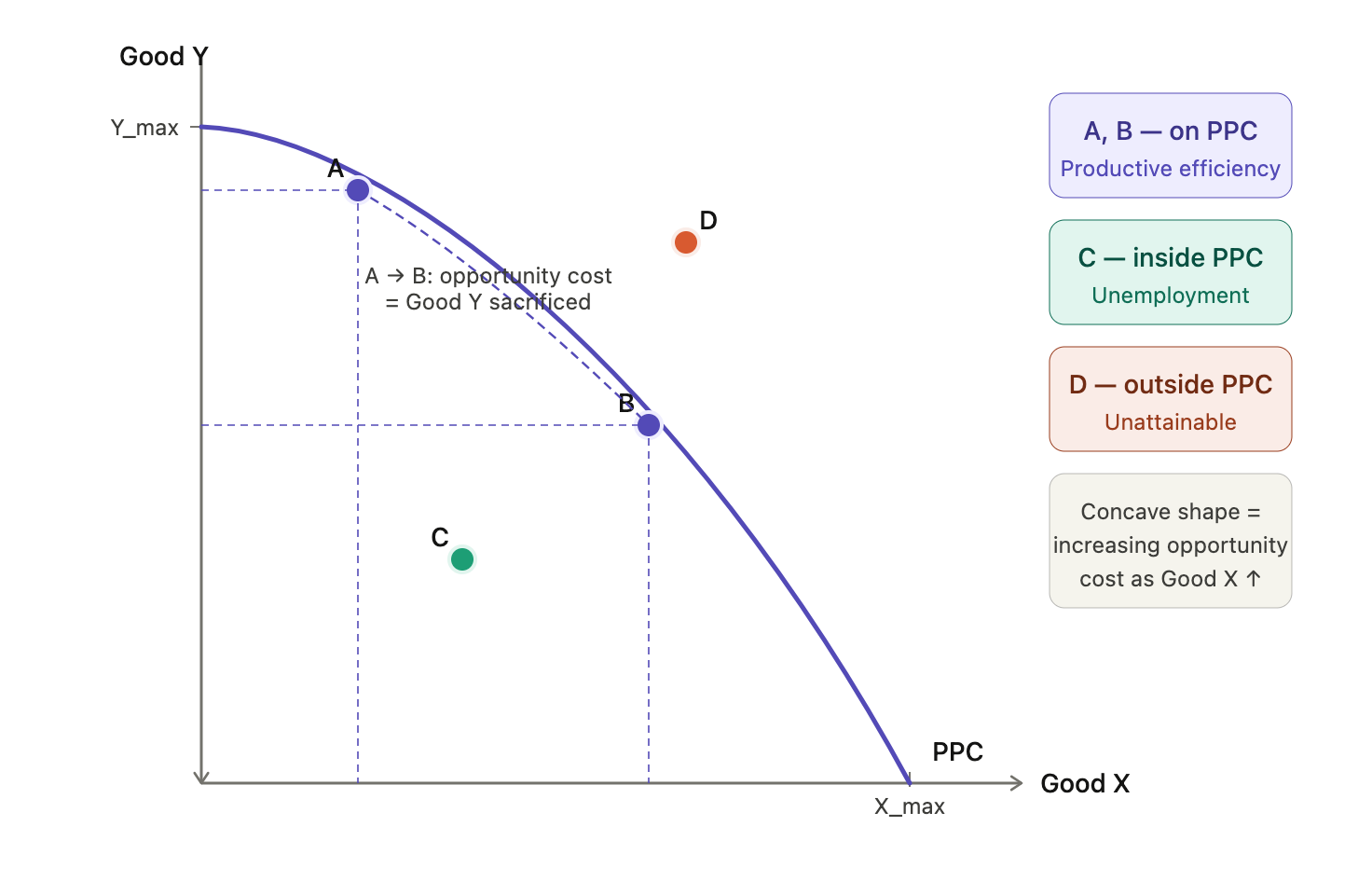

Definition: The Production Possibility Curve (PPC) shows the maximum attainable combinations of two goods that an economy can produce within a given time period, when all resources are fully and efficiently employed at a given state of technology.

Assumptions

- Only two goods are produced

- Fixed amount of resources, fully and efficiently employed

- Fixed level of technology

What the PPC illustrates

| Concept | Represented by | Explanation |

|---|---|---|

| Scarcity | Points outside the PPC | Desired but unattainable given current resources and technology |

| Choice | Points on the PPC | Economy must select one combination — it cannot be at all points simultaneously |

| Opportunity cost | Downward slope; movement along the PPC | To get more of Good X, must give up some of Good Y |

| Increasing opportunity cost | Concave shape | Resources are imperfect substitutes → opportunity cost rises as more of one good is produced |

| Productive efficiency | Any point on the PPC | Maximum output for given inputs |

| Full employment | Any point on the PPC | All resources fully and efficiently employed |

| Unemployment / Underemployment | Points inside the PPC | Resources idle or not used to their full potential |

Common mistake: A fall in unemployment moves the economy from inside the PPC toward the curve — it does NOT shift the PPC itself. Only a change in the quantity, quality, or technology of resources shifts the PPC.

Unemployment vs underemployment: Unemployment = some resources not used at all. Underemployment = resources employed but not to their full potential (e.g. an engineering graduate working as a taxi driver). Both place the economy inside the PPC.

Why the PPC is concave — law of increasing opportunity cost

Resources are imperfect substitutes — not equally suited to producing all goods. As the economy shifts more resources into producing Good X:

- Resources least suited to Good Y are transferred first → small sacrifice of Y

- As more X is produced, resources increasingly well-suited for Y must be transferred

- More and more Y must be sacrificed per additional unit of X

- ∴ Opportunity cost of Good X increases → PPC is concave

Example — increasing opportunity cost: Country M produces computers and textiles. As it shifts resources toward computers:

Combination Computers Textiles OC of 1 more computer R 0 42 — S 1 40 2 textiles T 2 36 4 textiles U 3 30 6 textiles V 4 23 7 textiles W 5 14 9 textiles Opportunity cost rises from 2 textiles (R→S) to 9 textiles (V→W). If opportunity cost were constant, the PPC would be a straight line.

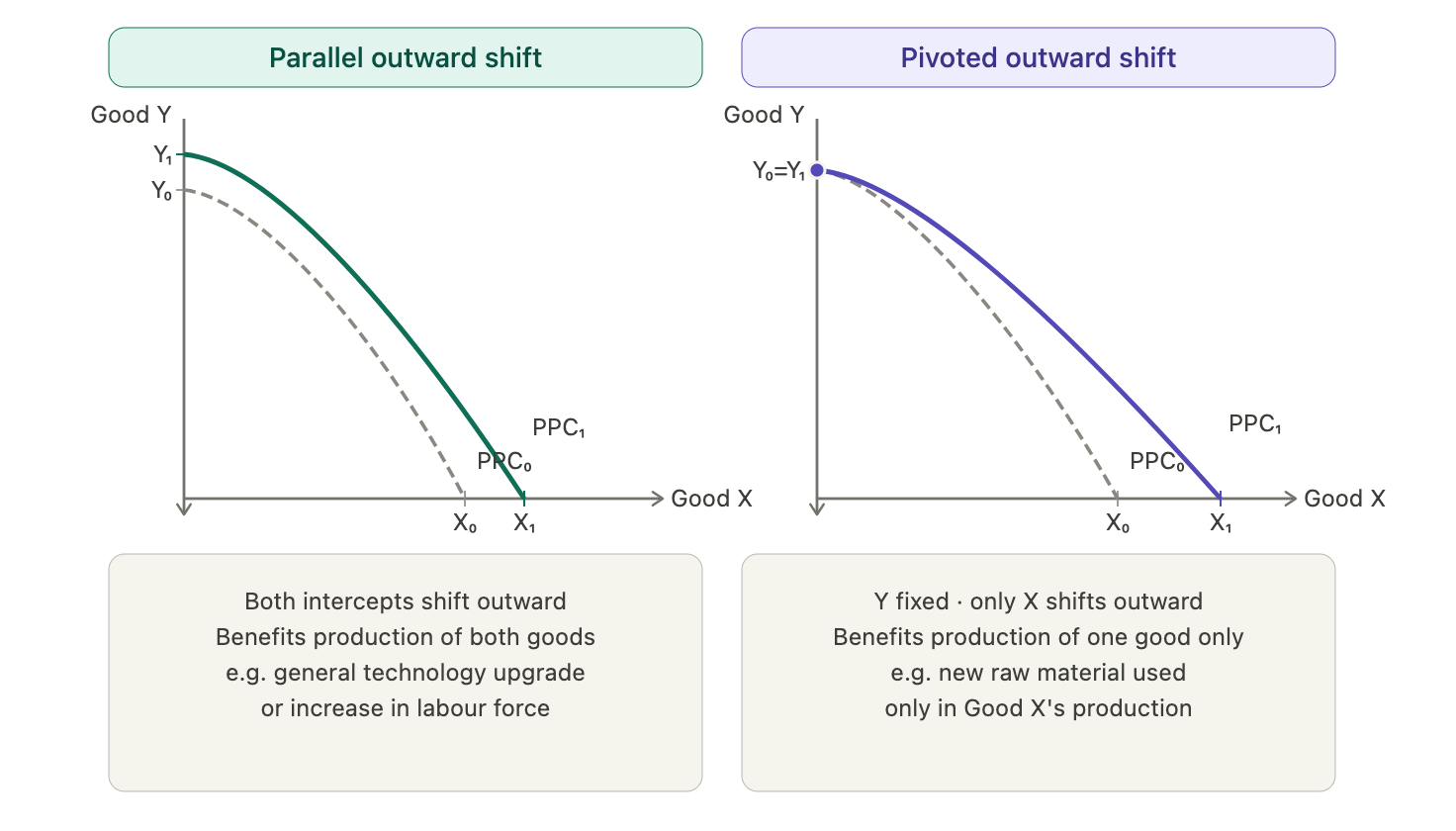

Shifting the PPC — changes in productive capacity (Q.Q.T)

An outward shift of the PPC = potential economic growth.

| Cause | Examples |

|---|---|

| ↑ Quantity of resources | More foreign workers (↑ labour); land reclamation (↑ land); increased investment (↑ capital stock) |

| ↑ Quality of resources | Better education/training (↑ labour productivity); improved machinery |

| ↑ Technology | Automation, new production methods through R&D → more output from same resources |

Memory aid: Q.Q.T. — Quantity of resources · Quality of resources · Technology

Types of PPC shifts

| Type | Cause | Effect on PPC |

|---|---|---|

| Parallel shift outward | Improvement benefits production of both goods equally | Both intercepts increase proportionally |

| Pivoted shift outward | Improvement benefits production of one good more | One intercept increases more; PPC pivots along one axis |

Economic growth & the PPC

| Type | Definition | On the PPC | How? |

|---|---|---|---|

| Actual growth | % annual increase in national output (GDP) | Movement from inside the PPC toward or onto the curve | Reducing unemployment or underemployment. Productive capacity does not change. |

| Potential growth | % annual increase in the economy's productive capacity | Outward shift of the entire PPC | Increase in quantity, quality, or technology of resources (Q.Q.T) |

Trade-off: consumer goods vs capital goods

| Type | Definition | Effect |

|---|---|---|

| Consumer goods | Goods that directly satisfy current wants (food, clothes, electronics) | Boost current standard of living |

| Capital goods | Man-made goods used in future production (machinery, infrastructure) | Drive future economic growth |

Key trade-off: More capital goods now → larger outward PPC shift in the future → higher future standard of living, but lower current consumption.

More consumer goods now → higher current standard of living, but smaller PPC shift → lower future productive capacity.

Efficiency & the PPC

| Concept | Definition | Location on PPC |

|---|---|---|

| Productive efficiency | Maximum output for given inputs; or given output at least possible cost | Any point on the PPC |

| Allocative efficiency | Combination of goods that maximises society's welfare | One specific point on the PPC |

Exam note: All points on the PPC are productively efficient. Only one point on the PPC is allocatively efficient. Points inside the PPC are neither productively nor allocatively efficient.

Key takeaways — 1.1.1e

- On PPC → productive efficiency + full employment

- Inside PPC → unemployment and/or underemployment

- Outside PPC → unattainable; illustrates scarcity

- Concave shape → increasing opportunity cost (imperfect substitutes)

- Unemployment does NOT shift the PPC — only moves the economy toward the existing curve

- Outward shift → potential economic growth (Q.Q.T.)

- Parallel shift → both intercepts move out equally

- Pivoted shift → one intercept fixed, one moves out

- Inward shift → loss or depletion of resources

- Movement toward PPC → actual economic growth

- Capital goods now → higher future growth, lower current living standards

- Consumer goods now → higher current living standards, lower future growth

- All points on PPC = productively efficient · only one specific point = allocatively efficient